The Business of Technology: Intel Q3 2007

by Ryan Smith on October 30, 2007 3:00 AM EST- Posted in

- Bulldozer

Intel by the Numbers

For our look at Intel's business side, we'll start with the barometer of the overall company status, the stock price.

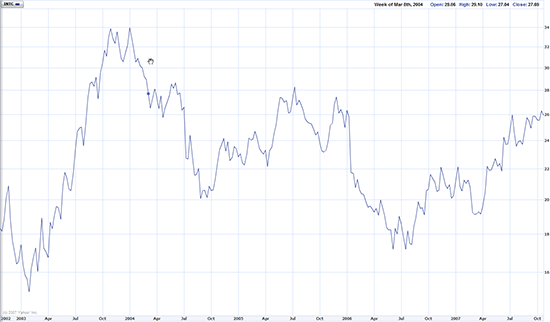

5 year stock history, courtesy of Yahoo! Finance

The stock market can be a very fickle beast, and not for reasons that immediately make themselves obvious. Depending on how far you want to go back in looking at their stock, you get two very different pictures. In the past year the stock has picked up over four points, for an increase of almost 22%, but if we go back a full 5 years Intel is effectively flat at best. In either case the stock is well above its lows of either period, but in the 5 year span specifically, it's well below its highs and is currently in a point that is effectively flat.

Intel's stock is further notable in that it is a dividend stock (a stock that returns regular dividends from profits) when many technology companies don't pay a dividend at all, rather opting to put all of their profits back into the company. This tempers the movement of the stock some, as investors will buy it with expectations of profiting from dividends and share price growth, rather than solely share price growth. This also means however that for better or worse, dividends are already factored into a stock price and that dividend growth is a required component of stock growth. Intel only pays out a very small fraction of its profits as dividends (on the order of less than a percent per quarter) but they are still not immune from the expectations created by dividends.

Dividends of course are a direct result of profits and revenue from the quarter, which is what we'll look at next.

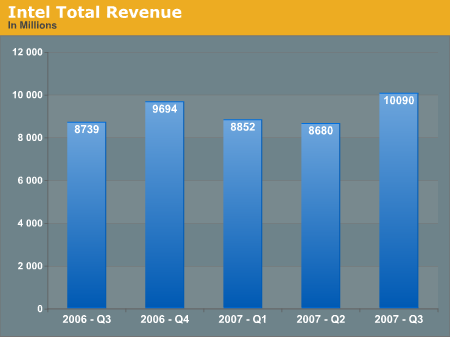

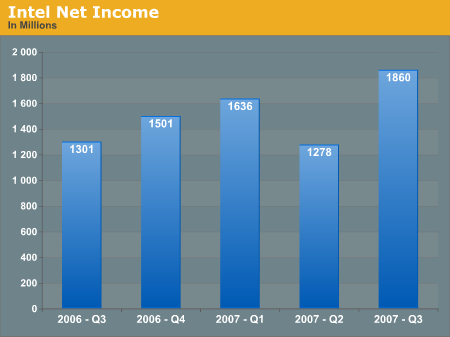

The primary reason we can call Intel a strong company is its revenues and profits. Intel hasn't been in the red for over a decade - even in particularly bad periods such as the post-dot-com bubble burst and their more recent troubles with the underperforming NetBurst architecture, the company has continued to record a profit. Thanks in a large part to their dominant position in the processor industry, they're one of the few technology companies that can claim such a long streak of profitability.

So with the revenue and profit in mind, why is their 5 year stock performance so poor? In a word: growth. There is a lot of concern in the investment community that Intel has completely tapped most of the market for computers globally. Although the computer is still nowhere near 100% saturation even in the most affluent nations like the television has become, there are few remaining groups that would be first-time computer buyers. Current computer owners have already settled into an upgrade cycle, but they're not likely to spend more on their next computer than their previous (adjusted for inflation where appropriate). For the stock to grow the company needs to grow; for the company to grow they either need their current consumers to consume more, or better yet find new consumers.

To get an idea of that situation, we have the basic product revenue breakdown from Intel's financial reports.

| Revenue By Business Group (In Millions) | |||

| Q3 2007 | Q3 2006 | Q3 2005 | |

| Digital Enterprise | 5204 | 4946 | 6370 |

| Mobility | 3971 | 3048 | 2970 |

| Flash Memory | 553 | 507 | 573 |

| All Others | 362 | 238 | 47 |

| . | |||

Unfortunately Intel reports this breakdown in terms of their business groups, which are not the same as their product groups. The processor revenue for example is split between the Digital Enterprise Group (PCs and servers), the Mobility Group (laptops and handhelds), and the much smaller Digital Home Group (set-top boxes and consumer electronics). But we do know what portion of the first two groups in particular are processor sales, which gives us an overall idea of what their processor revenue is like, and how it compares to the whole.

With the formation of their business groups in 2005, we only have just short of 3 years of comparable breakdown data, but there is a clear pattern in looking at it that much like Intel's stock price, their processor revenue is effectively flat, neither surpassing their highs or scraping their lows. This is in spite of their current technological advantage (more on that later) and has much to do with AMD. Intel's processor and chipset revenue is such a large part of the company that it effectively dictates the overall condition of the company financials, and right now Intel is still being held in check by AMD in some respects.

As we've touched on in our previous articles, AMD can't compete with Intel in the high end PC market with their current K8 architecture, but this hasn't stopped AMD from doing so in the low-end and server markets where they are stronger. Here AMD is fighting with pricing, cutting off Intel's avenues of growth through higher prices. The flat processor prices that result from this are the main thing being blamed for Intel's limited revenue growth. For this quarter in particular, it's an increase in total processor sales that buoyed Intel and helped them come in over analysts' expectations.

In response to the pricing pressures, and on the eve of AMD's Phenom launch, Intel seems prepared to play the pricing game for a protracted period of time. Intel has been shedding employees at a steady rate so far this year and will be continuing to do so for the rest of the year. The company started 2007 at 94,000 employees, and at this point is expecting to end it with 86,000. With the inability to control the pricing of the processor market, Intel has cited this as one of their key efforts to maintain and grow profits, by reducing overall costs and boosting the profit on each processor.

Finally, as Intel does from time to time, they're jettisoning a low-profitable/non-profitable business operation. Intel has left a number of memory businesses over the years, and until now their last memory business has been NOR flash, a less common form of flash memory that is used for direct application execution on devices like cell phones, thanks to its full random access capabilities. The NOR flash business has been losing money for some time now, and Intel has finally decided to cut their losses and spin off that business in a joint venture, mirroring what they did with their NAND business a couple of years ago. Intel's losses in flash memory so far this year have been particularly brutal (nearly three-quarters of a billion dollars), so this will further boost company profits, at a decent hit to lost revenue.

Going into the fourth quarter, Intel will also be doing so a further $150 million out of $250 million lighter, thanks to a settlement they've reached with ailing processor designer Transmeta over patent issues. The $150 million initial payment isn't a significant loss for Intel (it would be about 10% of their profits for Q4 2006), but it will temper most chances of a spectacular quarter.

13 Comments

View All Comments

BladeVenom - Tuesday, October 30, 2007 - link

Click on the Yahoo chart, then enter AMD, and compare.BladeVenom - Tuesday, October 30, 2007 - link

Or http://finance.yahoo.com/charts#chart1:symbol=intc...">LinkDfere - Tuesday, October 30, 2007 - link

Good Summary Article.I'm not sure if you have a description correct. I think "expected component" above as used in describing dividends are included in a pricing model as opposed to "required component" is more a appropriate economic term, unless "required component" is an actual economic term I have not been exposed to.

On a devious note, is it merely coincidence that everyone has a computer about time Moores law seems to be breached? I think not. I see someone's hand in this.